While it warms the cockles of my heart to see VC investors talking about selling companies, assessing them on the basis of their last 3-5yrs investing is currently near impossible. But the flip-side of this crash is that by the end of ~2025 we’ll have some useful datapoints on who the best new tech investors are (and which of the previous generation are more good than lucky).

I’m interested in who are going to be the best financiers for a couple of reasons: firstly because I’d like to invest in/with them and secondly because I’d like to build companies with their money. This probably marks me out as a little different than a regular LP, I care both about their track records but also their operating behavior around founders.

Although everyone is repeating (correctly) that most funds are a 10yr+ game, I think we’re going to see a very different exit environment emerge to what has been the recent norm. This is the ultimate test for VC investors who, as a generalisation, tend to be quite shy about talking exits and liquidity.

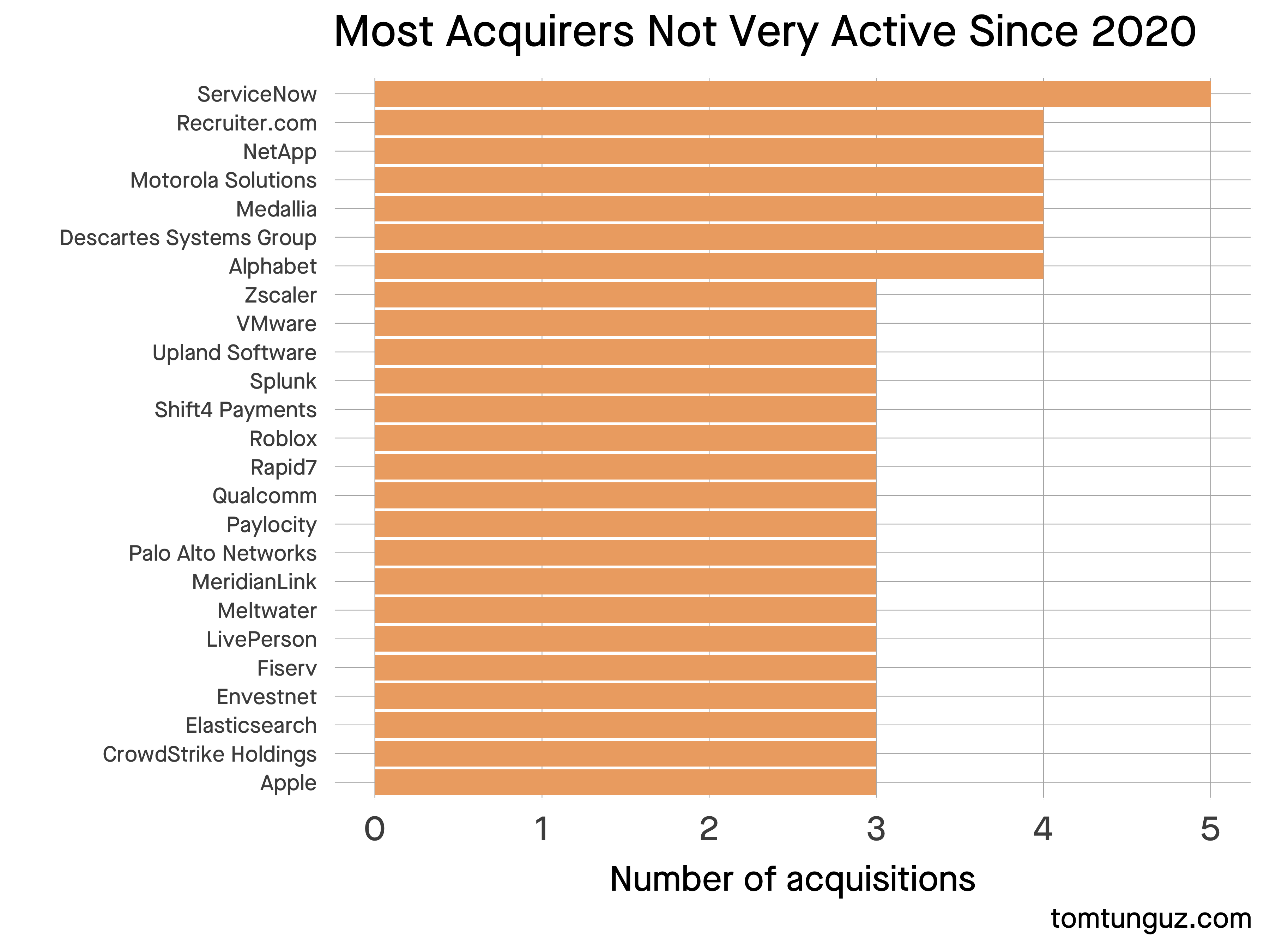

Public markets are obviously shut and although will (equally obviously) re-open at some point, it feels like a generation of PTSD has been laid down over the last twelve months. The regulatory environment appears to be making major tech deals harder to do for anti-trust reasons. And seems like the rate of acquihires is slowing, per Tomasz Tunguz’s data:

Towards the end of the bull market, we saw PE become the dominant buyer of technology companies. I haven’t seen a study on where the majority of VC fund distributions comes from but it should correlate. The catch us that PE buyers are usually looking for cashflow positive companies with robust unit economics.

Of course early stage companies don’t know where their exits might come from and should entirely be focused on solving problems. Investor behavior with founders during down-cycles are really where reputations and relationships are built. But you still also have a duty to return money to investors (I think everyone has once again learned about local maximum pricing). It’s a tricky balance.

So how are VC investors going to react? Broadly there are four signals that I’m watching for (and indeed are becoming visible already):

1. Giving up: The tourists will leave. There are going to be a lot of once-off funds (and fund managers).

2. Hunker down and increase engagement: slowing down investment pace and focusing on portfolios. This is the default behavior of any investor, good or bad. Things I would look for particularly around the top and middle quadrants of their portfolio engagement:

- Maximising value for middle performers: dealmaking, flexibility, actually talking about selling

- Creating value for expensive in-prices: making unpopular calls, helping management get difficult decisions done

- Activism: a pejorative term from the public market realm. I think it’s likely we’ll see a couple of Carl Icahn types emerge in the private markets over the next couple of years.

3. Expand: The volume of once-off portfolios creates an interesting opportunity for those fund managers who want to expand. In reality there will only be a tiny handful of windows like this in a professional investing career.

4. Adapt: expanding services and offerings up the value chain (boutique investment bank) and/or taking control of portfolio companies to drive liquidity (private equity). It’s a little early to point to concrete examples of this but A16Z feels like the closest candidate.

In bull markets, VC investing is dominated by conversations around in-price, position sizes and Total Value to Paid In (TVPI). The next five years is firmly about delivering Distributions to Paid In capital (DPI). As with the shift from visionaries to operators on the company-building side, I suspect the largest returns will be created by extremely proactive, executive producer style VC investors over the next few years.